The first era of Nigerian fintech rewarded speed. Companies that could process payments faster, designed cleaner interfaces, and deliver smoother onboarding captured users and attracted capital. But the market has moved. Speed and user experience remain necessary, but they are no decisive advantages. The next phase will be defined by whether a company has the right licence, regulatory approvals, data protection architecture, governance structure, risk controls, and compliance systems to launch, sustain, and scale its products. Customer demand alone does not validate a financial product. Regulatory Permission does.

Recent developments illustrate this shift. Flutterwave secured a microfinance banking licence to hold funds and deposits directly. Paystack acquired a microfinance bank licence as part of a broader restructuring into The Stack Group. Kuda obtained a national microfinance banking licence, removing the geographic limits of its earlier unit licence. These are not administrative steps. They are strategic product decisions that reshape each company’s position within the regulated financial system. This Tech brief examines how licences now shape product scope, how compliance affects product launch timelines, and what fintechs should do before launching new regulated products.

Licences as Product Infrastructure, Not Compliance Formalities

In fintech, a licence is not a procedural requirement. It is the core product infrastructure. A licence determines:

- what services can be offered

- how funds can be held or transferred

- whether deposits can be accepted

- whether credit can be extended

- whether direct access to settlement systems is possible.

Each licence category comes with defined permissions and obligations, including capital requirements, reporting standards, consumer protection rules, and AML controls. To learn more about the different fintech licences and their limitations, refer to our previous publications: Breaking into Fintech: Understanding the Key Licence Requirements and Limitations; Regulatory Mapping in African Fintech Sector, Understanding Commercial and Microfinance Banking Licenses in Nigeria.

In practice, a fintech’s product roadmap is shaped and limited by the licence it holds. This explains the strategic importance of recent licence acquisitions. By obtaining microfinance banking licences, companies such as Flutterwave and Paystack move closer to the balance sheet. This allows them to:

- hold customer deposits within a regulated framework

- strengthen user trust

- control over settlement flows more directly

- expand into credit and other financial services

Kuda’s national licence upgrade reflects the same dynamic. When a company’s operational scope outgrows its regulatory permissions, growth becomes constrained. Fintechs that combine payment capabilities with deposit-taking authority are therefore better positioned than those limited to payment initiation alone.

When Product Viability Meets Regulatory Reality

Traditional product-market fit focuses on customer demand (i.e., whether users want and will adopt a product). In regulated financial services, this lens is incomplete. Product viability must be assessed against both market demand and regulatory permissibility. A fintech product is only sustainable where it achieves regulatory product-market fit, which is alignment between its commercial model and the applicable legal and supervisory framework.

In practice, this requires a structured assessment across four core dimensions:

- Licensing Scope: The company must determine whether the proposed product falls within the scope of its existing licence. Where the product involves regulated activities such as deposit-taking, lending, insurance, or securities transactions, the company must confirm that it is duly authorised. Where gaps exist, the model must be restructured through a valid exemption, a licensed partner arrangement, or the acquisition of the requisite licence.

- Regulatory Engagement: Fintechs must assess whether the product triggers any form of regulatory engagement with the Central Bank of Nigeria (CBN), formal notification, sandbox participation, including prior approval, sandbox participation, or licensing. This determination should be made on a product-by-product basis, as regulatory treatment may vary across use cases.

- Data Protection Compliance: Because fintech products involve the collection or processing of personal data, it must be evaluated against the requirements of the Nigeria Data Protection Act. This includes assessing whether a Data Protection Impact Assessment (DPIA) is required and ensuring that privacy-by-design principles are embedded within the product architecture. Fintechs must also determine whether the new product necessitates updated consents, revised privacy notices, or new lawful bases for processing.

- Operational, Risk, and Structural Readiness: Product viability depends on whether the company’s control environment and corporate structure can support the product at scale. This includes governance frameworks, AML/CFT controls, cybersecurity safeguards, consumer protection mechanisms, dispute resolution processes, and regulatory reporting systems. It also extends to entity structuring as demonstrated by Paystack and Flutterwave. Multi-licence businesses must adopt holding company structures with ring-fenced subsidiaries and independent governance to ensure compliance with CBN’s requirement Specifically, each regulated subsidiary must maintain its own capital adequacy and governance framework.

A fintech product does not truly have product-market fit if it depends on a licence the company does not have, requires an approval that has not been obtained, processes customer data without proper analysis, relies on a partner in a way that undermines scalability, or scales faster than the company’s compliance infrastructure. Regulatory product-market fit is the test that separates products that can withstand regulatory scrutiny and scale sustainably from those that cannot.

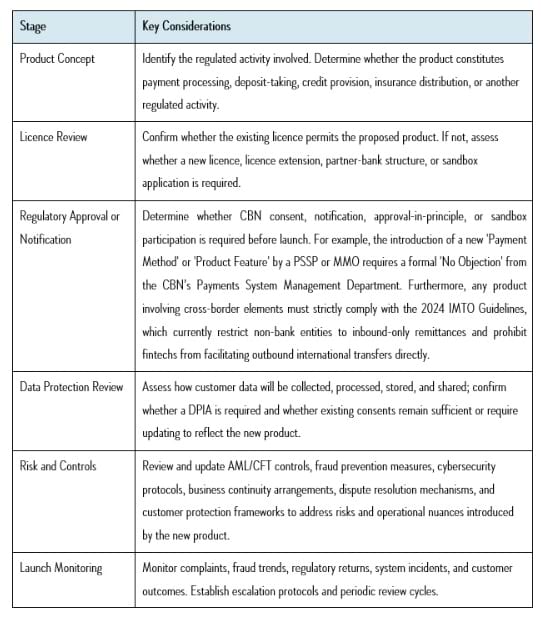

Roadmap for a Compliant Product Launch

Before launching a new product or feature, Nigerian fintechs should follow a structured regulatory product launch process. The following roadmap sets out the key stages.

Conclusion: What This Means

The role of fintech is evolving. Companies are no longer operating as front-end layers on top of traditional banks. They are moving into the core of the financial system. As a result, competition is shifting. As disruptors move from the periphery to the core of the financial stack, the battle for the customer is no longer being fought on UI/UX alone but on the strength of the underlying regulatory architecture.

The winners of the next decade will be those who recognise that licensing is not a hurdle to clear; it is a product feature.

To succeed in this environment, fintech founders must treat compliance as a foundational input, not an afterthought. Control over deposits, data, and infrastructure depends on regulatory alignment.

For investors and regulators, the key signal is also changing. Growth alone is no longer sufficient. Governance now matters equally. Fintech companies have demonstrated their ability to innovate quickly. The next challenge is durability.

Long-term success will depend not on speed, but on the ability to operate within and navigate complex regulatory systems. In this new phase, market leadership is determined not just by innovation, but by permission.