The Trap Door Strategy: How J. Crew Moved Its Crown Jewel Out of Lenders’ Reach

Introduction

When structuring a facility in leveraged finance, it is important to bear in mind that a lender’s protection is only as strong as the loopholes in the financing agreement.

Sometime in 2016, an American clothing retailer, J Crew Group Inc., amidst tremendous debt obligations, exploited a drafting gap in its financing agreements. The result of this gap permitted J Crew’s management to transfer its most valuable asset (the J. Crew Trademark, valued at USD$250 million) out of the reach of secured creditors for years, before the company eventually filed for bankruptcy in 2020. This strategy has since become popularly known as the “Trap Door” or “J. Crew Manoeuvre”.

Lenders often take comfort in the existence of a comprehensive security package, extensive covenants, and tightly negotiated credit agreements. However, the J. Crew Trap Door strategy demonstrates that a lender’s protection is not merely defined by the existence of security, but by the precision of the contractual framework governing the transaction. Like a house of cards, all it takes is one weak covenant to topple the entire structure.

In this edition of The Deal Talk, we examine the Trap Door strategy and the legal mechanics that enabled J. Crew to transfer its trademark, estimated at USD$250 million, out of the reach of secured creditors and why this matters to lenders, and borrowers alike.

The Story

In 2011, J. Crew Group Inc. (the “Company”) was acquired by private equity sponsors, TPG Capital and Leonard Green & Partners, in a leveraged buyout worth USD$ 3 billion. This transaction introduced a significant debt burden of about USD$1.6 billion onto the Company’s balance sheet.

Like many retail businesses of its time, J. Crew subsequently experienced operational headwinds driven by shifting consumer preferences and increased competition from fast-fashion and online retailers. By 2016, sales were declining, and J. Crew faced mounting liquidity pressure, with limited access to fresh capital and much of its asset base already pledged as collateral.

Further constrained by its existing debt obligations, J. Crew turned to its credit documentation, not to renegotiate, but to identify structural flexibility within the agreement itself. Relying on provisions relating to investments, restricted payments, and transfers to unrestricted subsidiaries, J. Crew transferred 72% of its core intellectual property into an unrestricted subsidiary and used those assets to incur new debt, impairing the value of existing secured creditors.

The Trap Door Mechanism: How the Asset Transfer was Structured

Rather than breaching its financing agreements, J. Crew’s lawyers found loose ends in Section 7.02 of the term loan agreement, which listed dozens of permitted investment baskets. Permitted investment baskets are specific categories of investments that a borrower is contractually allowed to make under a loan agreement without triggering a breach or requiring lender consent. They are negotiated carve-outs to the general restrictions in a loan agreement, designed to give borrowers operational flexibility for routine business activity. In J. Crew’s case, three baskets in particular became the architecture of the Trap Door:

The first was the General Basket, which permitted investments, including into unrestricted subsidiaries (subsidiaries that are not bound by the covenants of the loan agreement) up to the greater of USD$100 million or 3.25% of J. Crew’s total assets, plus an additional “Available Amount.” Notably, this basket placed no restriction on the type of asset that could be invested, meaning intellectual property was just as eligible as cash.

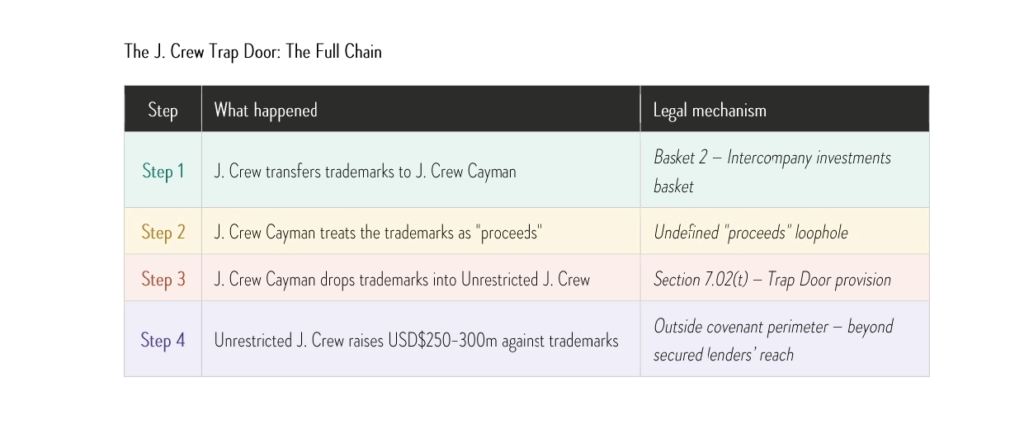

The second was the Intercompany Investments Basket, which permitted loan parties to make investments into non-loan party restricted subsidiaries, capped at the greater of USD$150 million or 4% of total assets, plus the Available Amount. It was this basket that J. Crew deployed to move its trademarks into J. Crew Cayman, a foreign restricted subsidiary deliberately structured as a non-loan party, meaning it sat within the covenant perimeter but outside the group of entities directly bound to the lenders.

The third — and most consequential — was the Non-Loan Party Investments Basket under Section 7.02(t), which became the Trap Door provision itself. This basket permitted non-loan party restricted subsidiaries, such as J. Crew Cayman, to make further investments into unrestricted subsidiaries, provided those investments were financed with the proceeds of investments made under the intercompany basket. It was this provision that enabled the critical second step: the drop-down of the trademarks from J. Crew Cayman into a newly formed unrestricted subsidiary, placing them entirely beyond the reach of secured creditors.

Individually, each basket appeared commercially reasonable and a routine accommodation for intercompany funding and operational flexibility. The danger lay not in any single provision, but in their sequential interaction. Used in combination, Baskets 2 and 3 created a two-step pathway through which J. Crew’s most valuable assets could be systematically moved outside the secured group without triggering a single covenant breach. As the image below illustrates, the chain of transfers was precise, deliberate, and entirely contractually permissible:

The J. Crew Trap Door: The Full Chain

This sequential use of the baskets is precisely what made the Trap Door so effective, and so instructive. It was not a single weak covenant that toppled the structure, but the unexamined relationship between several provisions that each, in isolation, seemed entirely defensible.

When a Definition Gap Becomes a Drafting Weapon

Compounding this structural vulnerability was a critical drafting omission in the definition section of the financing agreement, which never defined “proceeds,” even though that term appeared over 100 times. J. Crew ingeniously treated the IP itself as the “proceeds” of its initial investment into J. Crew Cayman. By this circular logic, the trademarks financed the very transfer that removed them from collateral. Without a definition of “proceeds,” J. Crew could stretch the term to mean “the investment itself,” thereby using Section 7.02(t) to transfer the IP outside the secured group. In short, a single undefined term — appearing over a hundred times in the agreement — became the lever that moved USD$347 million worth of assets beyond the reach of secured creditors.

Why this Matters: The Limits of Lender Protection

Today, the J. Crew Trap Door is relevant in leveraged financing not because it involved aggressive conduct, but because it was contractually permissible. It highlights a fundamental tension in leveraged finance: flexibility for borrowers often translates into risk for lenders. More importantly, it demonstrates that lender risk does not always arise from default or breach, but from compliance with poorly drafted provisions.

Practical Lessons for Lenders

- Define key terms with precision: The definition section in a financing agreement is not just aesthetics. The lack of definition or ambiguity in commercially significant terms, particularly those used repeatedly across operative provisions, can create unintended structuring flexibility. Definitions such as “proceeds,” “investments,” and “Permitted Transactions” must be tightly drafted and internally consistent.

- Contractually ring-fence core assets: Financing agreements should expressly restrict the transfer of material assets, especially intellectual property, outside the collateral package, unless subject to the lender’s consent or equivalent safeguards.

- Scrutinise investment and restricted payment baskets: Individually reasonable baskets can become problematic when used sequentially. Lenders and their lawyers must assess how provisions interact in practice, not merely in isolation.

- Limit unrestricted subsidiary flexibility: The ability to designate and capitalise unrestricted subsidiaries should be carefully constrained, particularly where such entities can incur structurally senior debt or hold key assets.

- Focus on structural protection, not just documentation: The J.Crew transaction shows that the real risk is not just what a borrower can do in breach, but what it is allowed to do under the agreement. Lenders must therefore look beyond the wording of covenants and consider how the structure can be used in practice.

Conclusion

The J.Crew Trap Door strategy remains one of the most instructive case studies in modern leveraged finance. It is a reminder that the strength of a financing structure lies not in the volume of its protections, but in their precision.

For lenders, the takeaway is clear: every covenant is a potential pathway. The question is not whether it can be breached, but whether it can be exploited.

The Finance and Projects Team at Tope Adebayo LP is comprised of seasoned, commercially savvy finance professionals well-positioned to assist clients in structuring and executing complex financing transactions, whether you are a Lender, Borrower, Trustee or Guarantor.